now loading...

The global economy is expected to slow down this year, and into 2023, as inflation, rate hikes, geopolitical conflicts and Covid-19 continue to create headwinds that are likely to result in the deterioration of underlying conditions for various business sectors.

In separate reports outlining their mid-year outlook for this year, Allianz Global Investors, Fitch Ratings and Coface reassessed their respective forecasts, citing risk factors that they think make a “hard landing” in 2023-2024 more likely.

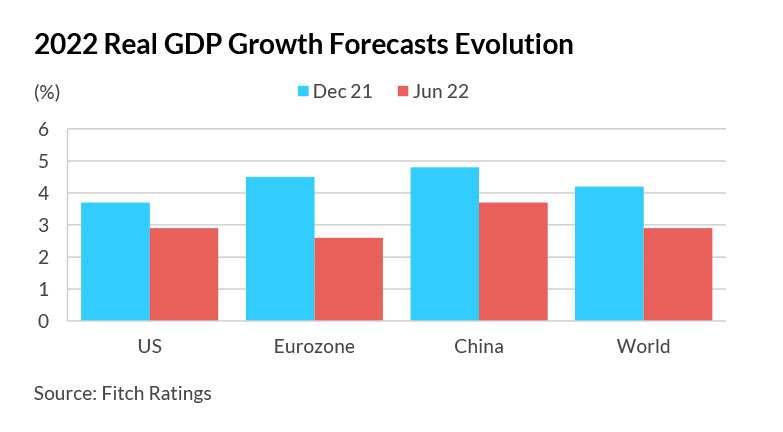

Fitch Ratings notes that while most of its sector outlooks remain “neutral”, there has been, on balance, a downward shift to reflect the worsening base case in what it believes to be a material deterioration in the global macroeconomic outlook.

“The Russia-Ukraine war and persistent coronavirus lockdowns in China are augmenting and perpetuating a global supply-chain crisis that has upended prior expectations for inflation, interest rates and growth,” says Justin Patrie, senior director at Fitch Ratings.

Coface has revised downwards its evaluation of 19 countries, including 16 in Europe – Germany, Spain, France and the United Kingdom in particular – while making only two revisions upwards, namely Brazil and Angola, in its Country and Sector Risk Barometer for Q2 2022.

At the sectoral level, Coface made 76 downward revisions and nine upward revisions, which it says highlight the spread of successive shocks across all sectors, both energy-intensive ones, including petrochemicals, metallurgy, paper, etc., and those that are more directly linked to the credit cycle such as construction.

“As the horizon continues to darken, the risks are naturally bearish and no scenario can be ruled out. The slowdown in activity and the risk of stagflation are becoming clearer. Q1 growth figures were below expectations in most developed economies. In addition, GDP in the eurozone grew only very weakly for the second consecutive quarter, with even a decline of -0.2% in France, due to a drop in household consumption against a backdrop of declining purchasing power. Activity also declined in the United States, hampered by foreign trade and the difficulties experienced by the manufacturing sector in replenishing its inventories. These figures are all the more worrying as the economic consequences of the war in Ukraine were just starting to bite,” according to the Coface Country and Risk Barometer.

For AllianzGI, its base-case view at the mid-year point indicates that within the next two years, the global economy will face a “hard landing”, or a state of very slow growth below potential. It also expects a US recession to emerge in 2023-2024.

“While we don’t anticipate 1970s-style ‘stagflation’, which is a toxic mix of slow growth and recessions in combination with double-digit inflation rates, we expect inflation to continue to surprise on the high side. Year-over-year inflation rates are likely to peak by the end of the year, provided we don’t experience another energy price shock, but it will take a long time ( at least three to five years, in the view of our senior investors ) for inflation to fall back to central banks’ targets ( usually 2% in the developed markets ),” says AllianzGI in its mid-year 2022 outlook.

Investor positioning

Given the widespread market uncertainty, investors are advised to diversify their portfolios by assembling a broader toolkit to smooth out volatility and take advantage of opportunities as they arise.

In equities, “quality value stocks that have healthy dividends may earn a premium price from investors amid higher interest rates, while quality growth stocks with strong balance sheets after a strong derating could be attractive as their growth profile helps them stand out amid poor global growth and an economic slowdown,” says Virginie Maisonneuve, global CIO equity at AllianzGI.

Thematic stocks such as energy security and food security, as well as artificial intelligence, cybersecurity and climate mitigation stocks, can also help investors reposition portfolios.

China equities can also be increasingly attractive, though volatility is likely to continue, since the country’s GDP growth of 4%-5% is notably higher than in major economies and many emerging-market economies. China is also less exposed to the negative effects of a strong US dollar and its central bank is loosening instead of tightening its monetary policy.

In fixed income, longer-duration sovereign bonds are beginning to look attractive in markets where rate hikes have been largely priced in, and where downside growth risks are set to become more apparent in the coming months, including in the US, Australia, New Zealand and Canada, according to Franck Dixmier, global CIO fixed income at AllianzGI.

“Among emerging markets ( EM ), selectivity is key. Geopolitical and supply-side pressures are sustaining underlying inflation, particularly in food prices, which represent a larger share of EM consumers’ inflation baskets. Among EM hard-currency bonds, high-yield spreads are wide. They may begin to come down as prices rise, which would make a compelling total return proposition for investors who already own these bonds,” says Dixmier.

In multi-assets, there may be opportunities for investors to re-enter the market as valuations have started to come down from what were too-rich levels, says Gregor MA Hirt, global CIO multi-asset at AllianzGI.

“We believe it may be wise to keep some cash on the sidelines for undervalued securities and select strategies. Commodity investments may help guard against rising inflation. In addition, gold may provide better diversification for equities than government bonds, at least for the time being. Commodity trading advisers are also benefiting from this environment, as they can short markets,” Hirt adds.